28 Jun The RBA On Crypto

Tony Richards, Head of Payments Policy Department, RBA, spoke on Cryptocurrencies and Distributed Ledger Technology at Australian Business Economists Briefing in Sydney.

He described the basics of Crypto, with reference in particular to Bitcoin, compares it with money, and concludes that many of these shortcomings of cryptocurrencies stem from their design around trustless distributed ledgers and the costly proof-of-work verification method that is required in the absence of a trusted central entity. In contrast, in situations where there are trusted central entities in well-functioning payment systems, there may be little need for cryptocurrencies.

He then goes on to explore the implications for central banks.

The Bank has been watching developments in these areas for about five years. Currently, however, cryptocurrencies do not appear to raise any major concerns for the Bank given their very low usage in Australia. For example, it is hard to make a case that they raise any significant concerns for the Bank’s mandate to promote competition and efficiency and to control systemic risk in the payments system.

Nor do they currently raise any major issues for the Bank’s monetary policy and financial stability mandates. There are only very limited links from cryptocurrencies to the traditional financial sector. Indeed, many financial institutions have actively sought to avoid dealing with cryptocurrencies or cryptocurrency intermediaries. So, it is unlikely that there would be significant spillovers to the broader financial system if cryptocurrency holders were to suffer valuation losses or if a cryptocurrency system or intermediary was compromised.

But given all the interest in cryptocurrencies or private digital currencies, people have inevitably asked whether central banks should consider issuing digital versions of their existing currencies. I can give you an indication of the Bank’s preliminary thinking on this issue, as outlined in December by the Governor in a speech entitled ‘An eAUD?’.

Currently if households wish to hold money, they have two choices. They can hold physical cash, which is a liability of the Reserve Bank, or they can hold deposits in a bank (or credit union or building society), which is an electronic form of money and is a liability of a commercial bank that is covered (up to $250,000) by the Financial Claims Scheme. Both forms of money serve as a store of value and a means of payment (assuming the bank deposit is in a transaction account).

Most money is already ‘digital’ or electronic in form. Currency now accounts for only about 3½ per cent of what we call broad money. The remaining 96½ per cent is bank deposits, which we might call commercial bank digital money.

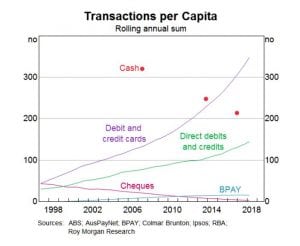

Furthermore, the use of cash by households in their transactions has been falling in recent years. This next graph shows there has been strong growth over an extended period in the use of cards and other forms of electronic payments. In contrast, the dots, which are from the Bank’s Consumer Payments Survey, show a significant fall in the use of cash. In 2007, cash accounted for nearly 70 per cent of the number of household transactions. Nine years later, this had fallen to 37 per cent.

Graph: Transaction Per Capita

Clearly, some households are moving away from cash and finding that electronic payments provided by banks better meet their needs. And this trend is likely to continue as the New Payments Platform (NPP), which launched recently, allows banks to offer better services to households – namely real-time electronic payments that give immediate value to the recipient, are easily addressed, are available 24/7 and carry lots more data than currently.

So the question is: ‘should the Reserve Bank introduce a new form of cash – an eAUD as the Governor called it – to give households an electronic payment instrument issued by the central bank for their everyday payments?’

Our current thinking is that there would not necessarily be all that much demand for an additional form of money in normal times, though this would presumably depend partly on design decisions such as the interest rate (if any) that would be paid on this money.

But to the extent that there was significant demand, particularly if this occurred at times of financial uncertainty with households switching out of the banking sector, there could be significant implications for the Bank’s financial stability mandate. There would also be implications for the structure of the financial sector – for example, it could result in reduced financial intermediation. We would need to think through these implications carefully.

So for the time being at least, consideration of a possible new electronic form of money provided by the Reserve Bank to households is not something that we are actively pursuing. Based on our interactions with our counterparts in other countries, it is also not front of mind for most other advanced economy central banks. An exception is Sweden, where the shift away from the use of cash is significantly more advanced than in Australia and elsewhere. Sweden’s Riksbank is studying the issues regarding the possible issuance of an e-krona and expects to report by late 2019.

However, as the Governor indicated in December, there might be a stronger case for considering a new form of central bank liability for use by businesses and financial institutions.

Here it is important to remember that the Reserve Bank already offers electronic balances to financial institutions in the form of Exchange Settlement Accounts (ESAs) at the Reserve Bank. These balances can be passed between financial institutions during the banking day, with the Bank keeping the official record (or the ledger) of account balances.[10] A key function of ESAs is that they provide banks with a risk-free liquid asset for settling payment obligations through the day, to prevent the build-up of large exposures that could threaten financial stability.

However, some stakeholders in the payments area – including some fintechs – have expressed the view that the introduction of another form of central bank balances could be quite transformative. They have suggested the issuance of a new form of digital money that would be accessible to businesses and could be passed around on a distributed ledger. They argue that the availability of another form of central bank settlement instrument could reduce risk and increase efficiency in business transactions. For example, it could allow the simultaneous exchange of money and other assets on blockchains. A central bank digital currency on a blockchain could potentially also enable ‘programmable money’, involving smart contracts and the simultaneous execution of complex, linked transactions.

Moving in this direction would involve two major changes to current arrangements: it would involve the introduction of a new form of settlement asset and it would presumably involve broader access to central bank money for non-bank institutions. Consideration of the first aspect will require an assessment of issues relating to the technology. Consideration of the second aspect would get into some of the issues that are relevant to thinking about giving households access to electronic central bank money, namely the implications for financial stability and the structure of the financial sector.

As we think more about a model along these lines we will be considering whether the benefits could be equally well facilitated by other means. For example, could there be commercial bank money on blockchains – say Bank X tokens, Bank Y tokens, and the like, rather than RBA digital settlement tokens? Indeed, some models have been sketched out whereby commercial banks would put aside ESA balances at the central bank or would put risk-free assets into special-purpose vehicles, and then issue credit-risk-free settlement tokens for use by their customers. We will also need to think about whether the possible use-cases that have been proposed really need central bank money on a blockchain, or if they might also be possible using other real-time payment rails – perhaps the NPP. At the moment, it does not appear that a strong case has emerged for us to provide this new form of central bank money, but we have an open mind.

From DFA